What is this story about the insurance part of the pension and the funded one?

From 2002 to 2020, an employee could write a statement about which form of pension calculation he chooses.

Everyone who did not write an application was considered to have chosen an insurance pension , which the state calculates according to its own rules.

For those who chose the funded formula , pension contributions were not 22%, but were divided into parts. Initially, 2-4% was allocated to the funded part; by 2008, the ratio was 16+6. 16% went to pay pensions to current retirees, and 6% went to the person’s personal pension account.

As a result, by 2013, 2.5 trillion “savings” rubles had accumulated in the accounts of pension funds, of which 1 trillion was in non-state pension funds.

There was even a program for co-financing a pension, when a person could transfer funds to his pension account, and the state added there the same amount as the citizen transferred. The program was widely advertised, but did not produce any special results - few people decided to put money aside for such a long time. Acceptance of new participants into the program was stopped on December 31, 2014.

How can you leave the NPF “Welfare” fund, take the money, and terminate the contract?

There are not many exit options:

- Come to the NPF office and write an application for termination of the contract and payment of the redemption amount, attaching your bank account details.

- Transfer the accumulated money to another non-state pension fund, for example to Sberbank.

On the first point - it is not for you if you are not ready to compete with hardened women from the personnel department (in most cases, the "Welfare" office = the HR department office of Russian Railways), who, caring about your future pension, will not allow you to deprive yourself such a benefit - additional payments in old age. They will use different technologies in order to convince you not to do such stupidity.

If you are purposeful and decisive, have worked for more than one year and understand everything, then you can act.

You ask to accept an application to leave the NPF “Welfare”, they start asking you if you are planning to quit, they say that we don’t leave without dismissal, you need to go personally to an appointment with your boss and in other ways they try to convince you.

One thing is not clear! If everything in this fund is wonderful, honest and open, everyone cares about your old age and wishes you a lot of money, why don’t they let people calmly leave this NFP? Why do you need to create a scandal to defend your right?

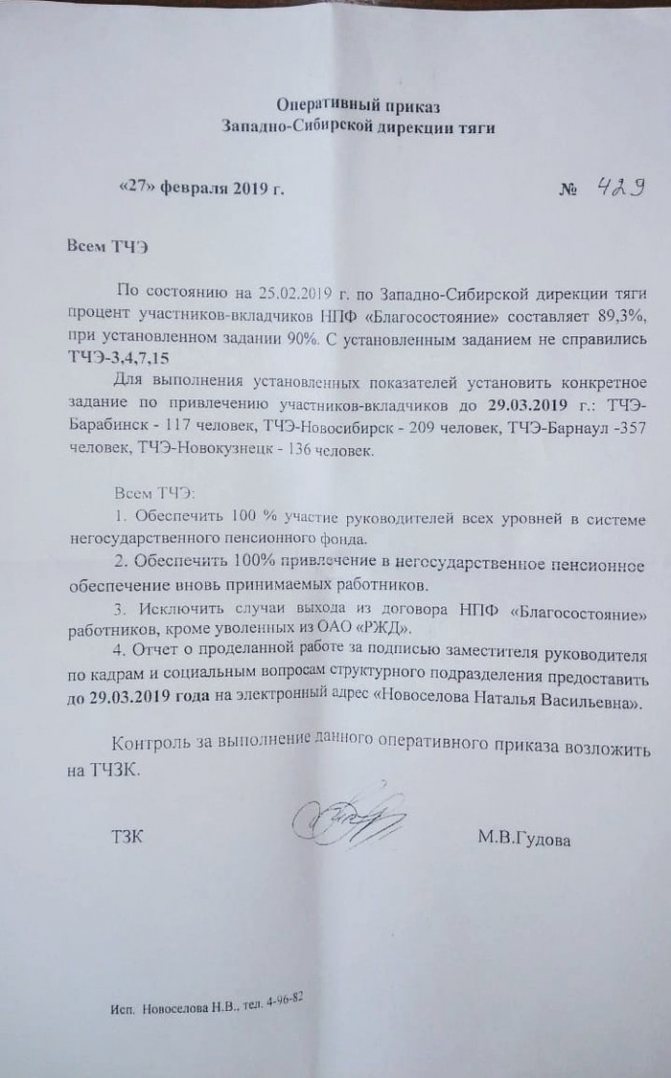

It all depends on your confidence. By and large, counterarguments can be given in the form of onlineinspektsiya.rf and the prosecutor's office. Perhaps after this you will be provided with a sample for writing an application. You write an application to both HR and accounting departments, attach the details of the bank account where the fund should return the money and wait 3 months. Then periodic agitation to join back will begin. The fact that personnel officers and management are interested in having as many workers as possible join the ranks of Blagosostoyanie is told to us by the following documents:

According to point 2 , everything was simple: You go to a Sberbank branch, enter into an agreement to transfer funds to them to the NPF, within a certain time the money from the NPF Blagosostoyanie migrates to the NPF Sberbank - you terminate the agreement at any branch of the bank - you take the money. But there is information that now the agreement must be concluded in the central office of Sberbank in Moscow - but I don’t believe it. Anyone in the know, please write in the comments.

The order of transitions between non-state pension funds

On January 1, 2020, a new procedure for changing the insurer for compulsory pension insurance (OPI) came into force, which can be either the Pension Fund of the Russian Federation (PFR) or a non-state pension fund (NPF).

Now citizens can submit an application to change their insurer only through the Unified Portal of State and Municipal Services (EPGU) or to the Pension Fund of the Russian Federation in person or through a representative with a notarized power of attorney. A similar procedure applies when submitting a notice of refusal to change insurer.To transfer pension savings from the Pension Fund to the NPF or from one NPF to another, it will still be necessary to conclude a compulsory pension agreement with the selected fund.

The transfer application must be submitted no later than December 1. There will be a “cooling-off period” until December 31, during which you can change your mind and stay in the same fund or choose another one. To do this, you will need to submit a notice of refusal to change the insurer or to replace it.

It should be noted that if the insured person submits more than one application for transfer to the Pension Fund within one year without first submitting notices of refusal to change the insurer, the Pension Fund will refuse to satisfy the second and subsequent applications.

The law provides for mandatory informing a citizen about the amount of lost investment income recorded in his account when submitting an application to change the insurer through the EPGU or directly to the Pension Fund.

Information about your applications and notifications, the date and method of submitting them, and the decision made can be found on the Public Services Portal. Notifications received by the Pension Fund in paper form will be independently registered by the institution’s employees on the portal, and they will be displayed in their personal account. At the same time, it will remain possible to obtain the specified information in person at the territorial branch of the Pension Fund or the selected NPF.

In addition, the Pension Fund of the Russian Federation, within one working day from the date of receipt of the application or notification regarding the change of insurer, will send this document to all interested non-state pension funds (from which and to which the citizen is transferring) through the interdepartmental electronic interaction system.

Changes in legislation are designed to eliminate the practice of illegally transferring pension savings to non-state pension funds using false documents and provide citizens with new information opportunities that will help them make more informed decisions when choosing or changing the method of investing their pension savings.

| Questionnaire-Application for connection to new services of the fund | SAMPLE: Questionnaire-Application for connection to new services of the fund |

| Personal information | SAMPLE: Profile information |

| Application for standard tax deductions | SAMPLE: Application for Standard Tax Deductions |

| Application for the appointment of beneficiaries (about changing the circle of persons indicated as beneficiaries and their shares) | SAMPLE: Application for the appointment of beneficiaries (about changing the circle of persons indicated as beneficiaries and their shares) |

| Application for refund of over-withheld personal income tax | SAMPLE: Application for refund of over-withheld personal income tax |

| Application to change the duration of payment of an assigned non-state pension | SAMPLE: Application to change the duration of payment of an assigned non-state pension |

| Application to change the method (details) of payment of non-state pensions and other funds | SAMPLE: Application to change the method (details) of payment of non-state pensions and other funds |

| Application for exemption from personal income tax for citizens of a foreign country | SAMPLE: Application for exemption from personal income tax for citizens of a foreign country |

| Application for recalculation of the amount of non-state pension | SAMPLE: Application for recalculation of the amount of non-state pension |

| Application for suspension/resumption/termination/restoration of payment of a non-state pension | SAMPLE: Application for suspension/resumption/termination/restoration of payment of a non-state pension |

| Beneficiary's application for payment/transfer of funds accounted for in the personal pension account of the deceased Investor/Participant/Participant-Depositor | SAMPLE: Application of the beneficiary for payment/transfer of funds accounted for in the personal pension account of the deceased Investor/Participant/Participant-Depositor |

| Questionnaire for an individual client |

Is it true that the funded part of everyone’s pension has been “burned out”? Where did this money go?

No. They lie in the pension funds where the person put them. For those who chose the state pension fund - at Vnesheconombank, for those who chose non-state funds - at the banks that were specified in the terms of the program. This money is replenished with interest depending on the profitability of the funds.

The phrase “funded pensions are frozen” means that since 2015, personal pension accounts have not been replenished; all your payments go to finance the pensions of current pensioners. Now there is no choice.

How to get

It was possible to choose a private pension fund into which a small percentage of pension contributions (6%) is transferred until 2014. After this, the program was frozen indefinitely.

If a working person born in 1966 has never written any application, he will not have a funded part of his future pension. All 22% of insurance premiums paid by the employer go to the state fund and are stored there.

In some cases, their employers made similar orders for their employees. If it suddenly turns out that the funded part still exists, then it can be managed - transferred back to the Pension Fund, to another private fund or to another financial organization. To find out in which fund the funded part of the pension is located, you need to contact the Pension Fund.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to find out how to solve your particular problem , contact a consultant:

8 (800) 700 95 53

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FREE !

The funded part is allocated to a separate independent pension. But you can receive these funds only after reaching the appropriate age. And only if the validity period of the savings account exceeds 10 years.

What if I open a bank account myself and save for my retirement?

This is please. But keep in mind that in our country there are no special “retirement” bank accounts.

They exist all over the world; these are special “long-term” deposits for 30-40 years.

The bank has separate conditions and benefits for such accounts; in addition, they are protected by a separate deposit insurance system throughout the world. In Russia it is simply a deposit on normal terms; that no one knows this money “for retirement” except you. Advice from Evgeniy Gontmakher, Doctor of Economic Sciences, member of the Committee of Civil Initiatives and one of the authors of the 2002 pension reform:

- Invest in yourself without waiting for payments from the state. Become the master of your own body. The approach “if I get sick, the government will help” is wrong. Get rid of bad habits, get a good education. Make savings, invest in real estate. Then there is a good chance that in your old age you will have a place to live and you will have money for medical care. The economic situation in the country is changing, so now is not too late to start doing this at 35.

But in general it is impossible to create an ideal pension system in a country with a non-ideal economy - they are connected.

There is a social pension and there is a labor pension - what is the difference? Which one is higher?

A social pension is a pension paid by the state to those who cannot be assigned a labor pension - that is, those who have never worked, a survivor's pension for children, and for some reason pensions for representatives of the indigenous peoples of the North are also included here.

Already now, the social old-age pension for those who have not had official work experience is assigned five years later than the usual labor pension - from 65 for men and from 60 for women.

The authors of the current reform propose paying a social pension from the age of 70.

The size of the social pension for disabled people is calculated individually. For disabled people of group III, it is about 4.5 thousand rubles, for disabled people of group I – a little more than 10 thousand. There is also a social supplement up to the subsistence level in the region.

Where does the money of those who do not live to retire go?

If a person does not live to see his pension, then the money that he did not receive for the current month can be received by his relatives who lived with him. In the future, monthly accruals of the deceased’s pension are not provided. In the absence of relatives, the money remains in the Pension Fund budget.

If a person fails to live up to the age of retirement, legal successors have the right to receive his cash savings accumulated in an individual account during his lifetime. From the budget of the Russian Federation, relatives of the deceased can receive social benefits for burial.

- How is coronavirus treated?

- Homemade watermelon rind jam

- Weight loss after 60 years is possible! You Just Need to Get Rid of These 8 Things