Basic concepts of Federal Law 168 on the funded part of a pension

Contributions to your personal accounts to form a pension in the future is a right that every citizen has.

Sources of such revenues:

- Employers.

- Personal contributions.

- Government funding.

Attention! The citizen receives the additional right to choose the policyholder with whom he will cooperate in the future.

Several options are available:

- Non-state pension funds.

- State.

- Management Company.

The right to change the policyholder is granted a maximum of once every five years. How deductions will occur depends on the individual characteristics of account management and cooperation. In the Pension Fund branch and in the Personal Account of State Services, you can obtain any necessary information.

Making payments involves submitting a corresponding application, which is supported by other evidence in writing. Additional requirements are imposed on those who apply for such payments ahead of schedule.

It is also useful to read: About Federal Law 173

The nuances of receiving the funded part of a pension in various non-state pension funds

Non-state pension funds are organizations licensed by the Bank of Russia and specializing in the management of pension savings. Their activities are regulated by the Federal Law “On Non-State Pension Funds”. According to the law, if the fund loses the funds of the insured person, the losses are reimbursed by the Deposit Insurance Agency.

Each fund operates in accordance with internal standards and rules, so the list of documents for receiving a funded pension may differ. In addition to the standard application, fund specialists may request original documents or notarized copies, and also ask to personally visit the organization’s office. Let's figure out what questions you may encounter when transferring and registering a pension.

At NPF "Gazfond"

NPF Gazfond has existed since 1994 and is currently one of the largest participants in the market. In 2020, RA Expert assigned the fund a ruAAA rating with a stable outlook, which indicates the high creditworthiness and financial stability of the organization. Pension funds are invested through Leader CJSC, which has been operating in the financial market for more than 26 years.

ATTENTION! You can get acquainted with general information about the fund, investment policy provisions, details, as well as the volume and structure of the portfolio by following the link in the relevant sections.

All documents required to conclude an agreement with a client, as well as the conditions for processing pension payments, are standard; the list can be viewed at the link. It also contains detailed information about possible schemes for accumulating and paying an additional pension.

At the moment, NPF Gazfond offers seven options:

- monthly lifetime payments, the amount of which is established by the investor (legal entity), and the purpose and procedure for payment is determined by the rules of the NPF;

- the duration, frequency of payments and the pension scheme are determined by the pensioner himself, but the procedure for appointment and payments depends on the rules established by the fund;

- the size and duration of payments is determined based on the accumulated amount; a minimum period (12 months) of payments is provided;

- the size and period of payments are determined by the pensioner, and the amount increases in proportion to the income received by the Pension Fund from investment activities;

- differs from others in that the decision on indexation is made by the Fund’s council;

- payments are made monthly, but what their size is is decided by the depositor (investor);

- The period of pension payments and the amount are determined by the NPF agreement with the pensioner, which is concluded for at least 10 years.

You can submit an application and copies of documents to receive a pension in several ways:

- in person by contacting the office of JSC NPF GAZFOND in Moscow or St. Petersburg;

- by mail, Simferopolsky Boulevard, 13, Moscow, 117556);

- contact an authorized representative of the depositor.

At NPF Otkritie

The second largest fund, NPF Otkritie, also has an AAA rating with a stable outlook. You can get acquainted with the management structure, reporting, and results of investment activities by following the link.

To enter into an agreement with a non-state pension fund for the management of pension savings, it is enough to submit an application in one of the convenient ways:

- through “Personal Account”;

- on the website by clicking the “Conclude an agreement” button;

- leave a request so that specialists will contact the future investor themselves;

- personally contact one of the fund’s representative offices with your passport and SNILS.

When concluding an agreement, the client will be able to choose the payment scheme, frequency and period of pension payments. Applying for a funded pension is simple - just show your passport and fill out the appropriate application.

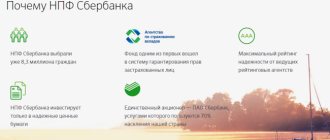

In NPF "Sberbank"

NPF Sberbank has been working in the pension market for 25 years and has offices in almost every city in Russia. The fund adheres to a conservative strategy, preferring to invest only in reliable securities. NPF Sberbank is a subsidiary of PJSC Sberbank, which is partially owned by the state.

The payment is assigned subject to the citizen reaching retirement age and the insured person submitting a certificate from the Pension Fund of Russia about the length of service, passport, SNILS and bank details for transferring funds.

You can submit documents in one of the convenient ways:

- in person to a Sberbank branch;

- in person to one of the NPF offices;

- through “Personal Account”;

- by mail.

At NPF "Safmar" and "Doverie"

NPF Safmar also specializes in pension savings management. You can find general information about the activities, licenses, and addresses of branches of NPF Safmar on the page.

ATTENTION! In 2020, NPF Doverie ceased its activities due to reorganization and merger with NPF Safmar. All obligations to clients were also transferred to NPF Safmar

You can apply for pension payments through your personal account or in person by submitting a standard package of documents (passport, SNILS, certificate from the Pension Fund and current account details). The procedure for registering a pension for clients of affiliated funds (“Trust”, “European”, “Regionfond”) is identical.

Who is entitled to a funded pension according to Article 4

Article 4 says that citizens of the Russian Federation and foreigners are entitled to payments if they meet the following conditions:

- Availability of pension insurance. Or participation in the system, which was designated as the PFR OPS.

- Availability of retirement savings. They were formed en masse by citizens born in 1967 and older. Another accounting period is 2002-2005. There are those who formed their savings on a voluntary basis outside of this time, by participating in special programs.

- Upon reaching the retirement age established by the general rules.

- Compliance with other requirements established by current legislation.

Using the savings of a pensioner, they are always given the opportunity to receive the following types of payments:

- Perpetual funded pensions. This is usually a priority form of using existing savings.

- One-time payments.

- Urgent savings payments. Their duration is determined by the pensioner. But the time is rarely set for more than ten years.

Basic provisions of the law on funded pensions

The funded type of pension is formed from regular contributions by the insured person's employer to the Pension Fund. This benefit is paid monthly on an ongoing basis and for life without expiration.

To start building a funded pension, you need to make an official choice in favor of this type of financial assistance . This right is given to citizens born in 1967, not older.

From the moment official work begins, and, consequently, the employer accrues pension contributions in favor of the employee’s future secure old age, the insured person has the right to choose whether to make all contributions to the accumulated pension, or to divide them into insurance and funded.

Please note: for those older than the above age, another program is provided under which you can make voluntary contributions to the accrued pension. For example, you can transfer all funds from maternity capital in favor of a secure old age. For an employed person, all insurance contributions are sent to form only an insurance pension.

Ensuring funded pension payments

The division of pension savings into two parts occurred about twenty years ago. Previously, the main source was deductions from salaries. After 2002, personal savings accounts belonging to citizens began to be used. The employer spends 16% of each payment on the insurance part of the pension. 6% is needed to form the savings part.

Reference! Contributions to the savings portion are stored in individual accounts. It is from these funds that benefits will then be paid to pensioners. Now those who retain official jobs are paying for them.

Conditions for assigning a funded pension

Insured persons can receive savings if a number of conditions are met:

- The emergence of rights to retirement, including early retirement.

- Availability of deductions on an individual personal account.

- Compared to the insurance pension, the funded pension amounted to 5% or more of the total amount.

If the amount is less than 5%, it means that funds can be received in the form of one-time transfers, in one amount.

Assignments for other types of collateral do not affect the funded part. If any changes appear, they are based on adjustments to the Federal Law, nothing else.

How does federal law determine the size of a funded pension?

The amount of payments is determined as of the day when the citizen applied to receive the money. The entire amount accumulated in the savings account is taken into account. The special part of the individual personal account is also carefully studied, if available.

Pension savings also include:

- Investment results.

- Maternity capital, part of which was spent in this direction.

- Contributions for co-financing.

- Contributions by the employer in favor of the insured person.

- Additional insurance premiums.

To determine the sizes use the following formula:

NP = PN/T

NP stands for the funded pension itself.

PN – pension savings, calculated from all the indicators mentioned earlier. T – the number of months during which the money will be received. The expected period may be shortened by a full year if the client applies for money later.

The procedure for installing and paying a funded pension

A citizen should not face any problems when assigning payments. It is enough to apply along with the application and other documents to the company in which he is currently served. You can use the help of PFRF or MFC employees to find out exactly where the funds are at the time you apply for payments.

Applications may be submitted by mail or through another citizen who has become the legal representative of interests. For example, when movement is difficult due to the current state of health.

Registration of the funded part of the pension requires the presence of the following documents:

- SNILS.

- Application according to the existing template.

- Civil ID of someone who has retired.

When registering insurance and savings parts at the same time, you will additionally need:

- Work record book and other documents to confirm work experience.

- Application for old age benefits.

Attention! The decision on the payments themselves must be made no later than ten days. Money is also transferred at the same time.

Payment of the funded portion to heirs in a lump sum

Accumulative pension provision appeared as a result of the reform of the pension system. Later, the procedure for formation, appointment and payments underwent a number of changes, and was finally established with the adoption of Federal Laws No. 351 and 424. In accordance with these legislative acts, each employer was obliged to contribute 6% of the salary of each employee to the savings fund. From these contributions, the accumulative part of the pension was formed, which workers could receive after retirement.

Each employee had the right to independently choose the fund to which contributions were sent. There were two options: either it was a state PF or one of the private funds. The money accumulated in citizens' savings accounts was invested by the fund in various profitable projects that brought additional profit. It was transferred in the form of interest to a savings account, increasing the amount available there.

In light of the deteriorating economic situation in the country, savings were frozen in 2015, and all employer contributions were redirected to the insurance fund. Thanks to this, the government was able to solve the problem of the shortage of financial resources to pay current pensions.

https://www.youtube.com/watch?v=ytcreators

Despite the imposed moratorium, existing pension savings have not disappeared anywhere. They continue to remain in the personal accounts of citizens and generate income from their investment. And upon reaching retirement age, the account owner has the right to receive this money. In addition, each person can independently form their own future pension by transferring certain amounts from their income to their account.

A one-time payment to pensioners from the funded part of the pension is made when the recipient meets a number of criteria. The main one is reaching the pension threshold. After a citizen receives an old-age pension, he acquires the right to assign savings payments. Another mandatory condition is that the total amount of savings, when calculating the monthly payment, is less than 5% of the assigned insurance pension.

All persons who have the right to receive a funded pension are established in Federal Law No. 167 and No. 424. The rules for the formation, conditions for receiving and types of payments of pension savings are also indicated there. Additional nuances are regulated by government regulations No. 1047 and No. 1048.

Who is entitled to

Any adult has the right to form pension savings. He can independently enter into an agreement with any fund, including state funds, open a personal account and transfer money to it. The following categories of workers have savings deposits in the state pension system:

- Females born in 1957-66, and males born in 1953-66. These citizens were participants in the savings program that operated in 2002-04.

- For all workers born after 1966, to whose savings accounts employers contributed 6% from 2013 to 2020.

- Women who decide to transfer the amount of maternity capital due to them to a pension savings account.

- Persons who have become participants in the program of state co-financing of voluntary savings contributions.

To apply for a funded pension, you need to provide a list of documents specified by law. It is the same for presentation to both state and private foundations. This list looks like this:

- Application requesting payments. It should indicate the form of receipt - urgent, unlimited, or one-time.

- General passport or other document replacing it.

- SNILS.

- Confirmation of periods of work experience. They are a work book or employment contracts.

- When receiving a funded pension for disability or loss of a breadwinner, you need certificates confirming the occurrence of this case.

Where to contact

It is necessary to apply for the assignment of the funded part of the pension to the fund where the citizen formed the amount of money. To do this, you need to submit an application to its employees, supported by the above documents. You can do this in several ways:

- By personally visiting the fund office at your place of residence.

- Sending the package of documents by registered mail.

- Through the district MFC. This option is possible if the account is opened in a state pension fund.

- Through the State Services website, again, if the savings are in the state fund.

- Through the official website of the fund.

After receiving a set of documents, fund employees have 10 days to familiarize themselves with it. If there is a shortage of any paper, they must inform the applicant about this, and he can provide the missing certificate within three months. After considering the application, if no obstacles to the assignment of a pension are found, then payments begin from the next month.

Pensioners have the right to receive their pension savings in a lump sum, regardless of whether they have completed their working career or continue to work. The main condition here is reaching the pension threshold and meeting additional requirements for the amount of savings (no more than 5% of the insurance portion).

Another feature of a funded pension is that in the event of the recipient’s premature death, it goes to his heirs. A citizen can indicate the person to whom he would like to leave the amount he has not received in his will. And in the absence of a posthumous expression of will, the money is distributed among all heirs in equal shares.

To receive the remaining savings, the heirs should contact the fund where the deceased’s savings were formed. The deadline for applying is no later than six months from the date of death of the account owner. The remaining pension savings can be received by the heirs only by paying a fixed-term pension to the deceased citizen.

Contributions sent by the employer for the employee during the period of work, as well as investments form the funded part of the pension. Payment of the funded component is carried out once a month from the moment the citizen officially registers the attained retirement age in a specialized organization. Citizens are given the choice of a pension company in which savings will be created.

At the expense of the employee’s salary, funds are transferred every month in the amount of 22%, where 6% can go (if the person wishes) to savings.

A citizen has the opportunity to direct all 22% of salary deductions to form an insurance pension.

To register savings savings, certain conditions must be met, the main one of which is reaching the retirement age limit (for 2020: for the female part of the population 55.5 years; for men - 60.5 years).

As soon as the funded pension is issued and assigned, it will be necessary to decide on the type of payment: fixed-term or lifetime. If a citizen is applying for a one-time payment, he will need to ensure that he meets the criteria.

These categories of the population may include people who:

- reaching the age limit corresponding to retirement age in the absence of the required number of pension points and length of service;

- payment of benefits in case of loss of a breadwinner in case of insufficiency of the required length of service;

- accumulated savings in the amount of less than 5% of the insurance pension.

The list of persons entitled to the right, conditions, terms and procedure for payment, and much more related to the funded pension is established by regulations: Federal Law No. 167-FZ, Federal Law No. 424-FZ, resolutions No. 1047 and No. 1048 (dated December 21, 2009). ). Due to numerous changes, you can familiarize yourself with the current editions on the legal systems.

Who is entitled to

According to the law, any citizen of the Russian Federation, as well as foreign citizens, has the right to create savings savings. However, in order to assign a funded pension, certain conditions must be met, which apply to certain categories of citizens:

- who have carried out work activities since 1967, taking into account that savings began to be formed at the expense of the employer (6% of the employee’s salary) until 2020.

- who made deductions in the amount of 2% of wages in the period from 2002 to 2004. Years of birth are: for men - 1953-1966, for women - 1957-1966.

- who are members of the Co-financing Program (deduction of funds from the state and citizen in a ratio of 1 to 1).

- who used family capital to create savings.

Persons whose age has reached the retirement age limit are paid at one time from their savings the amount accumulated throughout their life. However, the final decision on the amount of payment from savings remains with the Pension Fund employees.

Elderly citizens who have reached the age limit required for a pension and continue to work are applicants for receiving the funded part in the form of a one-time benefit.

The procedure for appointment and registration complies with generally accepted standards.

During his lifetime, every citizen has the right to choose heirs to whom savings savings will be transferred. For an official appointment, you will need to visit the Pension Fund to write a corresponding application. If a citizen does not have time to complete these actions before biological death, then the funds, according to the normative act, will be distributed among all persons who are relatives of the deceased.

In order for heirs to receive savings savings at a time, a personal (or through a representative, notarized) application to the pension organization is required no later than 6 months from the date of death of the citizen who formed the savings.

Can it be suspended and then resumed according to the law?

The transfer of monthly insurance amounts may be suspended if the following circumstances exist:

- The pensioner went abroad for permanent residence.

- Upon completion of the training period, lack of certificates in the case of loss of a breadwinner.

- The foreigner has overstayed the time when it was necessary to apply for an extension of the main document.

- They stopped receiving payments at the post office or from their bank account.

If there is no reaction from the citizen, the regulatory authorities have the right to refuse to pay any compensation at all.

You can also resume transfers. For example, when they submit a corresponding application, and also hand over documents that prove the position of the originator. After this, the citizen must be paid all amounts that he had not previously received.

How the law regulates the payment of savings. Pensions for those leaving the Russian Federation

When traveling abroad, a person is not deprived of the right to receive a pension. But there is a high probability of various technical problems arising. It is better to find out in advance about the rules by which savings are made in such cases.

Important! The main requirement is to avoid delays in receiving your pension for six months or more. If this happens, you will have to contact the supervisory authority again to resume payments.

Pensions are also paid to those who have moved for permanent residence.

But even here it cannot be done without a number of conditions:

- Annual confirmation that the citizen remains alive.

- Notification of the Pension Fund about a new place of residence.

- Lack of indexing.

- Refusal of regional allowances.

- Submission of certificates confirming the availability of official work or its absence.

- Certificates of permanent residence outside the territory of Russia.

- Submitting applications for departure.

Most often, when abroad, money is immediately transferred to bank accounts.

The Ministry of Finance has published a bill on a new type of funded pension

The launch of the new system is scheduled for 2021, according to materials from the Ministry of Finance. First Deputy Chairman of the Central Bank Sergei Shvetsov clarified that the system will start working no earlier than mid-2021, Interfax reported.

Basic option - payments for 15 years

Read on RBC Pro

How economic shocks are changing people’s habitual patterns of behavior How a mysterious startup intends to create a quantum computer faster than Google How to adapt to new consumption models - Nielsen recommendations Lean management tools: kaizen session

The pension payment under the SPP will be assigned:

- or when a citizen reaches the standard retirement age (65 years for men and 60 years for women);

- or after 30 years from the date of commencement of payment of pension contributions under the GPP - whichever comes first.

It must be paid monthly and calculated using the formula “amount of pension payment = total amount of participant’s contributed funds / 180”, adjusted for the result of placement of pension reserves. This means that the basic payment option is a pension payment for 15 years. But participants will be given the right to choose other options other than the basic one, according to the explanatory note of the Ministry of Finance.

Shvetsov clarified that “there is a proposal to make the payment stage as a sliding term payment”: the first calculation of the pension is made based on the fact that it is paid for 15 years, but after one or two years a recalculation occurs based on investment income and what has already been paid ; in two years - a new recalculation, etc.

There is also the possibility of early payment of savings if a participant in the system is diagnosed with diseases from the government-approved list of socially significant ones. The payment is made in the amount of treatment costs, but not more than the amount of savings made.

If the profitability of placing pension reserves turns out to be negative, the NPF will be obliged to make up for the negative result from its own funds. In the event of the death of a GPP participant, his accumulated unpaid funds are included in the inheritance and are inherited on a general basis by relatives.

Register of participants

The register of GPP participants will be maintained by the pension operator - the National Settlement Depository (NSD), which has the status of a central depository. The register must include, in addition to personal data, information about the amount of pension contributions, the amount of contributions paid, suspension and resumption of payment of contributions, etc.

If NSD unlawfully refuses or evades entering and changing information in the register, it will face administrative liability - a fine of 700 thousand to 1 million rubles, follows from the companion bill, also presented by the Ministry of Finance.

In the explanatory note, the Ministry of Finance notes that the GPP will give citizens the opportunity to “create, through personal contributions, additional sources of financing pension income in the non-state pension system with incentive support from the state and strengthening mechanisms for protecting and guaranteeing pension rights.” Participants in the GPP scheme will be provided with a “wide range of rights,” the department emphasizes.

How many people will save through GPP?

How many Russians will agree to participate in a completely voluntary pension savings scheme and what percentage they will contribute from their income is not yet clear. Shvetsov admitted that “from the point of view of replenishing accounts,” the story will not immediately become widespread.

A Levada poll conducted in the summer showed[/anchor] that 63% of Russians would not like to make additional contributions to a non-state pension fund in addition to the existing mandatory employer contributions. Only 29% of respondents expressed their willingness to contribute additional money from their income. This is due to the lack of free money among the population and distrust in the system, in which the rules of the game are changing quite quickly.

The presented bill looks like a compromise between the requirements of different blocs of the government and the Central Bank, Anton Tabakh, chief economist of the Expert RA rating agency, tells RBC. In his opinion, as a result, “a safe system can be built, not very straining on the budget, but also not very attractive to the upper middle class and wealthy Russians, for whom it is, in fact, designed.”

“Under these conditions, the upper limit [for participation in the state pension program] is the number of people who are connected to the voluntary non-state pension system, that is, about 6 million,” Tabakh suggests. “I think that realistically, over a period of five years, there will be from 3 to 5 million people regularly making contributions,” the expert said.

“GPP is a small button that is sewn onto the pension system,” says CEO Evgeniy Yakushev. In essence, it is proposed to do what can already be done within the framework of non-state pension programs, individual and corporate, he says. Forecasts for the population's participation in the state-funded program are still disappointing, because in the current conditions there are very few people who can afford to save on their own, argues Yakushev.

The Ministry of Finance estimates the maximum coverage of the SPP system at 72.5 million people - employees and self-employed. If we superimpose the data from a June survey by the Levada Center on the willingness of Russians to make additional pension contributions with Rosstat data on the distribution of the population by average per capita income for 2020, you can get an upper estimate of the annual volume of pension contributions under the SPP - about 1 trillion rubles, RBC calculated.

Other significant points of the law

Pension savings are paid to legal successors if the death of a citizen occurs before the total amount is assigned or before adjustment. An exception to the rules is made only in the case of maternity capital and the results of its investment.

Age and working capacity do not affect the right of citizens to receive compensation . This applies to children and closest relatives in line.

If there are no relatives, no money is paid to anyone at all. They are taken into account as part of the reserve in relation to current pension insurance.

The citizen himself has the right at any time to submit an application indicating the persons to whom the pension can be transferred in the event of death. In the absence of an application, funds are distributed in equal shares among relatives belonging to the same line. It is allowed to use electronic portals to submit applications regarding the determination of the circle of responsible persons.

It is imperative to indicate in what shares the money is distributed. If the legal successor missed the deadline for applying for payment, but there was a serious reason for this, he can also draw up an application so that this time is restored.

Until the end of 2020, citizens were obliged to make a choice in favor of the funded part of their pension if they had a desire to take part in this system. A separate period was established, before the end of which working citizens had to submit relevant applications. If there was no application, then only the insurance part was automatically generated.

At the same time, in any case, the citizen retains the right to write a refusal to participate in the formation of his savings. After that, all the money is directed only to the insurance part. But even after this step, you can replenish your savings account, just on your own. The selected company invests all collected funds in one direction or another. Payments occur according to the general procedure.

While abroad, a citizen can receive several types of payments at once:

- Additional monthly support for WWII veterans.

- Additional payments for labor merits.

- State pensions, with the exception of social pensions.

- Insurance pensions.

Such payments can be processed without any problems without even returning to Russia. It is enough to send an application and other documents to the regulatory authority to prove your position. Don't expect approval the first time.

Attention! There is a high probability that additional document requirements will arise. It is better to take care in advance of obtaining a card where funds will be credited. Then fewer difficulties arise.

How to receive the funded part of a deceased relative’s pension

In the event of the death of an insured citizen, his pension savings are also inherited. The pensioner has the right to send his insurer (PFR or NPF) an application in which he can indicate the persons (successors) to whom money will be paid in the event of his death. If such an application was not submitted to the fund, then the money is inherited in accordance with current legislation.

It is worth noting that the right to inherit the remainder of the mat. capital and income from its investment after the death of the insured person is owned only by the father (adoptive parent) of the child in connection with whose birth the mat was received. capital (provided that he is not the stepfather of a previous child, whose order was taken into account when issuing financial capital). And in the event of the death of the father (adoptive parent), the right to receive money will then pass to the child (or children in equal shares). If there are no persons who can inherit the savings, they are transferred to the Pension Fund.

1 667